Disclaimer: This article is intended for informational and educational purposes only and should not be considered as financial advice. The views expressed are those of the author and are not intended to serve as a replacement for professional financial advice. Individual financial circumstances vary, and we recommend consulting with a qualified financial advisor to discuss your specific situation.

Key Learnings:

- Discover How Banks Really Work: Learn the fundamentals of the banking system, including how banks use your deposits to fuel loans, investments, and the economy.

- Interest Rates Demystified: Gain clarity on how interest rates are determined and their impact on your savings and loans, empowering you to make informed decisions about where to store your money and when to borrow.

- Credit Insights: Understand the critical role of credit scores and how banks assess your financial behavior, offering strategies to enhance your creditworthiness and secure better loan terms.

- Navigating Bank Types for Your Benefit: Explore the diverse landscape of banking institutions—from retail to online banks—and how choosing the right one can align with your financial goals, whether you're managing personal finances or planning for a family's future.

- Strategies for Maximizing Banking Benefits: Equip yourself with practical tips on leveraging banking services to your advantage, including how to use different account types and digital tools to streamline your finances and build wealth.

Banks are not your friend.

Welcome back to the Wealth Intelligence Academy, where we're on the sixth leg of our financial literacy building journey, at the end of which, the above sentence will make a lot more sense.

As you embark on this journey, one truth becomes strikingly clear, as it did with me: sometimes, the most familiar things are the least understood. Banks, for instance, are these financial fortresses that hold our hard-earned cash and fuel economies, yet they are often shrouded in mystery and poorly understood by the regular person in the street.

What really happens behind those polished counters and in the digital vaults of online banking?

This sixth installment of our Basic Module series aims to pull back the curtain on the banking system, a topic as essential as it is enigmatic. Whether you're a young professional taking your first steps into financial independence or a young family planning for a prosperous future, understanding how banks operate is crucial. We'll embark on a journey to demystify the banking system, stripping away complexity and delivering the essence of what you need to know.

You may believe these fiscal fortresses to be impenetrable, but that is not the case - this is not a risk-free kind of rodeo. I remember a time when the importance of understanding banking risks hit home hard - a lesson as bitter as that two-day-old coffee you forgot on your desk. It was during the Greek financial crisis, a period marked by turmoil and uncertainty.

Like many, I watched in disbelief as the stability of banks came into question. It was a stark awakening that echoed the cautionary tales of my grandfather, who, by the way, swore by the 'backyard bank' for years. Perhaps he wasn't that far off the mark, after all. You see, banks are not there to be your friends, and protect your money. Their primary objective is to generate profit from you.

So let's prepare to navigate the maze of banking with the precision of a cat burglar and the skepticism of an internet conspiracy theorist. Here's what's in store:

- We'll dissect the mystical world of interest rates and credit loan, where your money grows or shrinks depending on which side of the equation you find yourself.

- We'll peek into the seemingly clandestine operations of different bank types—unveiling the roles of central banks, commercial giants, and those elusive online platforms that promise banking nirvana from the comfort of your sofa.

- Because we're all about safety here (unlike my grandfather's backyard banking strategy), we'll delve into the thrilling world of banking regulations and how they're the unsung heroes keeping your savings from becoming a cautionary tale.

- We'll delve deeper into banking strategies for families so you understand how to best make use of these modern wonders

- And finish off by getting more "worldly" and taking a peek to see how banks operate in other parts of the world.

Ready to roll?

I. The Inner Workings of Banks: Understanding Your Dollar's Journey

So, how do banks work?

At their core, banks are the economic equivalent of social network platforms, but instead of connecting friends, they're financial institutions that match people's money with those who need it. Banks gather deposits from those of us who are, let's say, financially well-endowed at the moment and lend them to those in a bit of a pinch or looking to grow a business.

In the simplest of terms, a bank's job is to hold your money and that of businesses, and then use that money to help the economy grow. It acts as the middleman between those who want to save their money and those who need to borrow it.

Why do banks exist?

Well, imagine trying to find someone trustworthy enough to hold onto your life savings under their mattress, or on the flip side, trying to find a stranger willing to lend you money to buy a house. Banks were created to solve these problems by providing a secure place for savings and a reliable source for loans. The absence of banks would increase risks for both savers and borrowers due to the lack of a regulated system for financial transactions and the absence of deposit insurance.

The concept of banking is as old as civilization itself going back to the time of the empires, but the first recognized bank in the modern sense was Banca Monte dei Paschi di Siena, founded in 1472 in Italy. It was established to offer financial services to the underserved, particularly to provide loans to the poor. This historical move was essentially about creating a system where money could be pooled for the benefit of the community, proving that the fundamental role of banks has always been to support economic activity and stability. It remains the oldest surviving bank in the world [1].

Now, your deposited money isn't just stashed in a vault for a pampering session. It earns interest, which is the bank's way of saying, "Thanks for letting us borrow your cash, here's a little something for your troubles." (subtle emphasis on "little" there, but that's a story for another day).

On the flip side, banks charge interest on the money they lend out, which is how they make a profit. This cycle of depositing, lending, and earning interest is what keeps the economy's wheels turning.

Personal Finance and Banking

So what do you banks actually do for you personally, aside from sending an avalanche of paper statements and enticing credit card offers. They're not just glorified piggy banks or impersonal loan sharks (yes, yes I can hear some of your groaning at that with your dad jokes, but that's what they're meant to be).

Banks offer a suite of services designed to support individuals and families in managing their money more effectively. Remember those articles we navigated together on budgeting, savings, and the tightrope walk of debt management? Banks are your co-stars in those sagas. They offer the savings accounts that are supposed to make your money grow (at a pace that can sometimes feel glacial), giving you a little pat on the back with interest.

Here are examples of some of the services banks offer in supporting your financial growth.

Savings Accounts:

- Earn interest over time, transforming deposits from your savings account into a growing asset.

- Directly supports our discussions on the importance of savings.

Budgeting Tools:

- Banks provide apps and online tools for tracking spending and managing finances efficiently, echoing the strategies outlined in our article on budgeting.

Loans and "Good Debt":

- Easy access to loans for significant life investments, such as homes or education, aligns with our advice on leveraging debt positively.

- Banks evaluate your creditworthiness, a concept we explored in depth in our debt management piece, determining your access to favorable loan terms. Your credit score, a reflection of your financial behavior, influences eligibility and terms, underscoring the importance of maintaining a good financial standing.

More on loans and interest in Section II.

The Journey of the Dollar

To explain this in a different way (as everyone learns differently), let's follow a young dollar in their journey through the bank lifecycle. (I'm sure you all understand the above principles, this is really just an excuse for me to be creative!)

In the grand narrative of banking, every dollar—let's call this one 'Horatio' for fun—plays a starring role. Horatio's journey from deposit to investment illustrates the bank's pivotal function as an economic catalyst. His first day on the job at the bank was the beginning of an epic saga.

Upon entering the bank, Horatio was more than just currency, he was potential. Greeted not with a party or confetti, but with the solemn nod of a teller, Horatio was quickly whisked away into the vaults. But Horatio wasn't destined to gather dust. No, he was about to be lent out to someone with a vision so bold it could only come from the most eccentric corners of the Californian entrepreneurial world: an alpaca yoga retreat.

Yes, you heard right. Horatio found himself funding a man's dream to combine the tranquility of yoga with the, uh, unique presence of alpacas. It's the kind of business plan that makes you wonder if genius and madness are indeed two sides of the same coin. Yet, Horatio wasn't one to judge. He was one to enable.

As the alpaca yoga retreat took off (to the surprise of skeptics and the delight of alpaca enthusiasts everywhere), Horatio began to multiply. Each yoga session, now inexplicably popular, turned a profit, part of which was used to pay back the loan with interest. This is where Horatio's magic really happened: through the alchemy of banking, he didn't just return to the bank, he brought friends.

Imagine Horatio, returning to his original owner, but now he's not alone. He's accompanied by additional dollars, clones of himself, each one a testament to the successful fusion of alpacas and yoga. This multiplication was the result of his investment journey, growing through the interest paid on the loan he facilitated.

This tale of Horatio is a microcosm of how the banking system fuels dreams, supports the economy, and ultimately, benefits us all (of course some more than others, but hey, that's life). Every deposit, like Horatio, has the potential to fund the next unlikely success story, and in doing so, grow.

In the sequel to this story, we find out when Horatio gets lost on his adventures and the bank demands more Horatios from you - but let's stay positive shall we?

The South Park team does an "alternative" take on explaining Horatio's adventures with the bank

Taking a step away from Horatio and understanding the essential roles banks play, let's dive into how they impact your pocket through interest rates and credit systems.

II. Interest Rates and Credit Systems: The Backbone of Your Financial Decisions

Navigating through the financial landscape, interest rates and credit systems stand as the critical elements influencing every aspect of personal finance. Building on our exploration of how banks integrate with personal finance, this section delves deeper into the intricacies of interest rates and the pivotal role of credit in banking, offering insights crucial for informed decision-making and revealing their outsized impact on your wallet.

The Mechanics of Interest Rates

Interest rates, essentially the cost of borrowing money or the reward for saving it and "allowing" the bank to use to lend to others, are determined by the economic wizards at the central bank based on complex interplay of factors including central bank policies, economic conditions, and market demand for credit. These rates, represented as percentages, directly impact your financial well-being, influencing how quickly your savings grow and how much you pay for loans.

- Determining Interest Rates: Imagine a room full of economists armed with data, trying to predict the future of the economy, while sipping on their 150 year aged bourbon. Central banks set benchmark interest rates that guide the overall level of interest rates in the economy. From there, individual banks adjust their rates for savings accounts and loans based on factors like risk, inflation, and market competition.

- Impact on Savings and Loans: Higher interest rates make loans more expensive but increase the earnings on savings accounts. Low rates? Cheap loans, but your savings might as well be stuffed under the mattress for all the good they're doing there.

- Compound vs. Simple Interest: Ah, compound interest, my fifth love (hello wife and kids) and the Eighth Wonder of the World. It's the reason your savings can grow exponentially, stacking interest on top of interest. Simple interest, on the other hand, is calculated only on the principal amount, offering a linear growth path. You can learn more about my love affair with the compound effect and its power in turning modest savings into substantial wealth over the long term in our Savings module.

- Fixed vs. Variable Rates: Fixed interest rates remain constant over the loan period, offering predictability for budgeting but potentially missing out on lower rates if the market changes. Variable rates, conversely, can fluctuate based on market conditions and central bank policies, potentially offering lower rates initially but with the risk of increasing over time.

Credit in Banking

Credit scores and credit utilization play central roles in the banking sector, determining your eligibility for loans and the terms you'll receive. These components of your financial profile are crucial for banks in assessing the risk of lending to you.

- Role of Credit Scores: Your credit score is a numerical representation of your creditworthiness, based on your history of borrowing and repaying loans. It influences not just whether you can get a loan but also the interest rate you'll pay. High scores get you into the VIP section of banking, with low-interest loans and respectful nods. Low scores? Welcome to the back of the line, where loan sharks and high-interest rates lurk

- Credit Utilization and Risk Assessment: Banks use credit scores to assess the risk associated with lending to an individual. Credit utilization, or the ratio of your current revolving credit (like credit card debt) to your total available credit, is a key factor in determining your score. Maintaining a low credit utilization ratio is seen as indicative of responsible credit management, positively affecting your score and thereby improving your loan conditions [2].

It's crucial to note that the concept of credit scores, while prevalent in the U.S., doesn't universally apply in the same manner globally. For our international audience, let's explore how different regions assess financial reliability.

- In countries like Australia, the approach to evaluating creditworthiness diverges from the U.S. model. Instead of relying solely on a credit score, Australian banks and credit institutions conduct comprehensive credit assessments (CCR). These evaluations consider your income, employment stability, existing debts, and even your savings habits. It's a more holistic view of your financial health, beyond just how you've handled debt in the past, akin to having a financial resume

- While the concept of credit utilization is a significant factor in credit scoring systems like those in the U.S., in places without a singular credit score metric, lenders may look more at your debt-to-income ratio. This ratio offers insight into your ability to manage new debt given your current income, reflecting a pragmatic approach to assessing borrowing capacity.

Regardless of the system in place, the underlying principle remains the same—banks and lenders are keen on minimizing risk. Whether through a credit score, CCR, or debt-to-income ratios, the goal is to ensure that loans are offered to individuals who demonstrate financial responsibility and the ability to repay.

III. Exploring the Diversity of Banking: Types and Services

As we pivot from the nuances of interest rates and credit systems, it's essential to navigate the vast safari of banking types and services, to discover where your money can best grow wings or at least avoid being eaten.

This diversity caters to the varied needs of individuals, families, and businesses, making it crucial to choose a banking partner that aligns with your financial goals and lifestyle.

Various Bank Types

Navigating the world of banking without falling asleep at the wheel means knowing what each institution brings to the table:

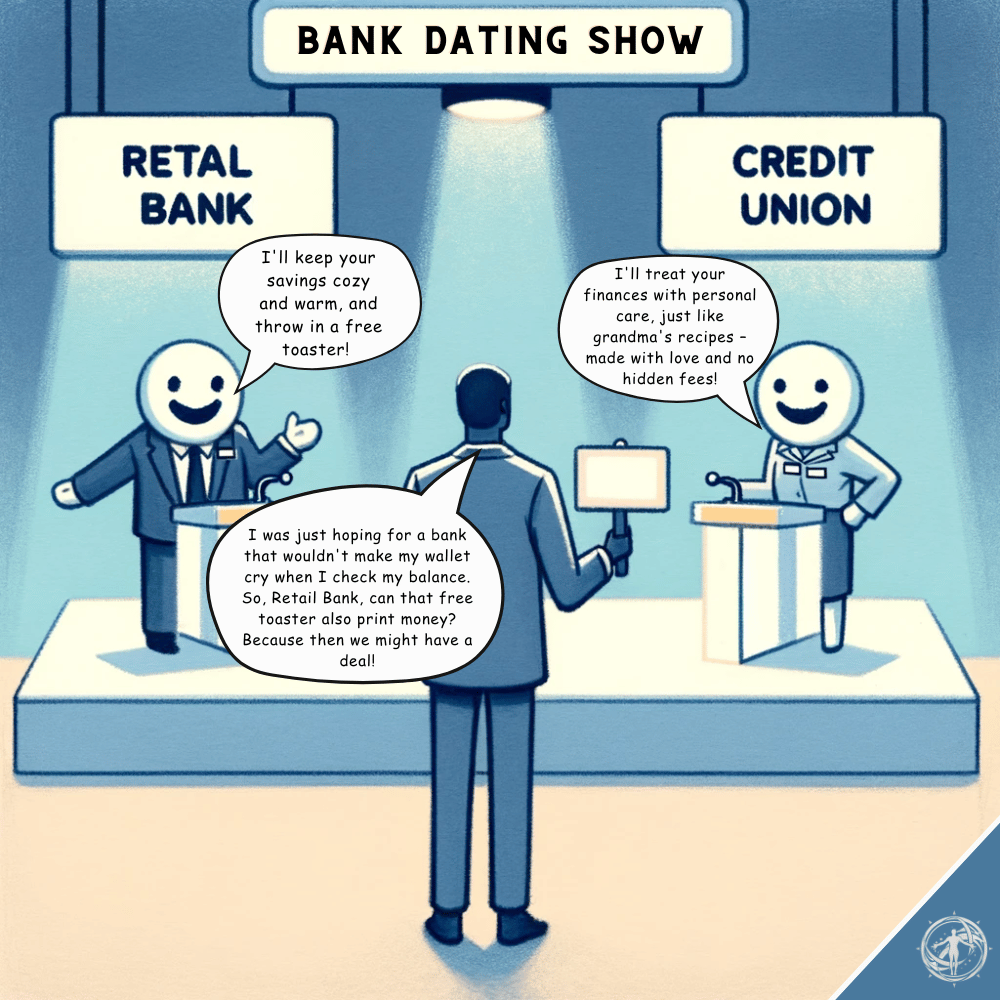

- Retail Banks: Catering primarily to the general public, retail banks are perhaps the most familiar to the average consumer - it's your traditional bank. They offer a broad spectrum of services including checking accounts and savings accounts, loan and mortgage services, and credit cards. It's where you and I go to deposit our paychecks, wishing the interest rates were as high as our hopes - but let's face it, the interest rates on savings are about as satisfying as a limp salad. Examples include Citibank.

- Corporate or Commercial Bank: The steak houses for the business world, offering meatier financial services with a corporate price tag. They're where businesses go to borrow money, getting loans and cash management services that make retail banking look like child's play. Their services extend beyond daily banking to include credit services, cash management, commercial real estate, and trade finance. Notable examples are JPMorgan Chase and Bank of America, which also operate substantial retail banking divisions.

- Investment Banks: The alchemists, turning corporate strategies into gold, or so they claim. They’re like the elite matchmakers in high society, specializing in complex financial services for corporate clients, investment banks assist with underwriting, M&A activity, and other financial transactions. They serve large corporations, other financial institutions, pension funds, governments, and hedge funds. Morgan Stanley and Goldman Sachs rank among the largest U.S. investment banks [5].

- Central Banks: Distinct from the types mentioned above, central banks oversee a nation's monetary policy and money supply, aiming for economic stability. They regulate the banking industry but do not mingle with the common folk. The U.S. Federal Reserve and the European Central Bank are prime examples [5].

- Credit Unions: Unlike traditional banks, a credit union operates on a first-name basis, where profits are a taboo word, and the focus is on member benefits. They offer routine banking services but are typically smaller and more community-oriented, often providing more favorable rates and lower fees due to their tax-exempt status. Great if you like your banking with a side of moral superiority.

Tailoring Services to Needs

Choosing the right bank involves matching its services with your specific financial needs and preferences. It's like dating—what are you in it for? A fling with high interest rates or a long-term relationship with low fees?

Here are some considerations for you when deciding:

- Assessing Your Financial Goals: Determine whether you're seeking comprehensive personal banking services, investment opportunities, or business banking support. Look beyond the appetizers. What services do you actually need? If you're eyeing investments, a retail bank trying to be your broker might leave you wanting more.

- Service and Fee Comparison: Beyond the basic interest rates, compare fees, service charges, and the accessibility of banking services, including online and mobile banking options.

- Lifestyle Considerations: For those who prefer digital access or travel frequently, online banks or large national banks with extensive ATM networks might be preferable. If personalized service and community involvement are priorities, consider local banks or credit unions. On the flipside, if you don't care whether a bank knows the name of your dog, and just want someone to look after your money, send this criteria higher in the priority queue.

- Investment Opportunities: Many banks, especially retail and universal banks, offer investment services. Evaluate these options based on your risk tolerance and financial objectives, ensuring they complement your overall investment strategy. Just because a bank offers investment options doesn't mean you should take them. Sometimes, the best financial advice is to keep your banking and investing separate, like oil and water, or pineapple and pizza (that last one is controversial, I know - especially if you're Italian).

Choosing the right bank might not spark joy, but it shouldn't cause despair either. You're now equipped with the knowledge to make informed decisions about where to bank. Why not take this opportunity to assess whether your current bank is the right fit for your needs?

Before you do, read our next step on ensuring our journey through banking is as safe as it is fruitful.

IV. Banking Regulations and Consumer Safety: Protecting Your Finances

After unraveling the types of banks and the services they offer, it's time to armor up and dive into the fortress that keeps the financial dragons at bay: banking regulations and consumer safety.

Yes, this is where the excitement of banking meets the thrill of paperwork and policy, because as we covered earlier, banking is not a risk-free operation. Navigating this world of banking regulations might seem like you need a law degree, but it's really about understanding the safety nets put in place to protect you, the consumer.

Regulatory Framework and Consumer Protection

The banking world, thankfully, is more like a well-regulated sport rather than a free-for-all gladiator fight, with referees ensuring fair play and protecting the spectators—aka, you, the consumer.

Here’s who’s holding the whistle:

Key Regulatory Frameworks

- Federal Deposit Insurance Corporation (FDIC): Think of the FDIC as the financial knight in shining armor, offering deposit insurance to save bank depositors from losing their money if the bank decides to take an unscheduled sabbatical (i.e., fails). Up to $250,000 per depositor, per bank, is covered, making it less terrifying to stash your cash in a bank [6].

- Other Notable Referees: The Federal Reserve and the Office of the Comptroller of the Currency play pivotal roles in overseeing banking practices, from how much money banks should have in their vaults to how they conduct their business. They ensure banks are playing by the rules, maintaining enough cash to avoid turning a game of Monopoly into real-life financial distress.

Let's look at an example. Let's say Jane Doe deposits $10,000 in her savings account. Thanks to the FDIC, if her bank were to unexpectedly close, she wouldn't lose her money. She's protected up to $250,000, ensuring her peace of mind.

Similarly, when she opens her account, the bank must provide her with all the details about fees and interest rates, ensuring transparency, much like a food label listing ingredients and nutritional information.

Significant Banking Laws:

- Imagine a world where banks could do as they please, like a toddler with no bedtime. Acts like the Truth in Savings, Electronic Fund Transfer Act, and the Expedited Funds Availability Act ensure that banks can't play fast and loose with the terms of your account or make you wait eons to access your deposited checks. It's the rulebook that makes sure the game of banking is played fairly [7].

- Several acts, such as the Home Mortgage Disclosure Act, Equal Credit Opportunity Act, and Truth in Lending Act, are in place to protect consumers and require fair treatment and full disclosure in credit and lending practices [7].

- The Fair Credit Reporting Act regulates the use of consumer credit information, while the Fair Debt Collection Practices Act governs the practices of debt collectors [7].

Global Perspective on Banking Regulations

While we've delved into the U.S. regulatory landscape, spotlighting heroes like the FDIC, it's pivotal to recognize that the drama of banking regulation isn't a solo act performed on the American stage alone.

Around the globe, various nations have their own versions of the FDIC, each playing a crucial role in keeping the financial system from going off the rails.

- International Counterparts to the FDIC: For instance, the United Kingdom has the Financial Services Compensation Scheme (FSCS), protecting depositors up to £85,000 [10]. Similarly, Canada's Deposit Insurance Corporation ensures up to CAD 100,000 [11], and Australia's Financial Claims Scheme covers up to AUD 250,000 [12]. These international safeguards underline a universal truth: no matter where you bank, there's likely a safety net, albeit with its own set of rules and coverage limits.

- Evolving Global Regulations: Post-2008 financial crisis, the Basel III regulations were introduced internationally, setting more stringent capital requirements and risk management protocols for banks worldwide. This global handshake agreement among banking regulators aims to fortify banks against the shocks that previously sent economies spiraling [13].

Lessons from History

At this point, some of you are in a state of disbelief thinking that banks can never possibly fail.

Diving into the annals of financial history uncovers many examples of past failures. The below episodes serve as critical lessons on the importance of rigorous regulations and the consequences of their absence when it comes to banking:

The Savings and Loan Crisis (1980s):

Ah, the 80s, a time of questionable fashion and even more questionable banking practices.

The Savings and Loan (S&L) Crisis, which predominantly unfolded in the late 1980s, was like the financial world's awkward teenage phase: full of risky investments and a glaring lack of supervision. It was a financial disaster rooted in a mix of deregulation, poor lending practices, and speculative investments. Initially, S&L institutions were restricted to taking deposits and making mortgage loans.

However, deregulation in the early 1980s allowed them to expand their services, venturing into riskier investment areas without sufficient expertise or oversight. Coupled with an unstable interest rate environment, these practices led to massive failures.

By the end of the crisis, over 1,000 S&Ls had failed, costing taxpayers approximately $124 billion, according to the FDIC. The crisis underscored the dire consequences of inadequate regulation and oversight, leading to significant reforms in banking supervision.

What followed was a fair bit of regulator reform to prevent any sequels from transpiring in the future.

a brief history lesson on the S&L failure if you have time (source: Slope of Hope)

Recent Bank Runs (Early 21st Century):

The digital age has not been immune to the age-old phenomenon of bank runs, as evidenced by the rapid withdrawals from banks like Silicon Valley Bank and Signature Bank in recent years. These more recent collapses serve as modern-day ghost stories for the financial sector, showing that confidence in banks is as fragile as your grandmother's china.

These runs often stem from a crisis of confidence among depositors, exacerbated by the viral speed of information dissemination through digital channels. For instance, the collapse of Silicon Valley Bank in 2023 highlighted the fragility of banking institutions in the face of rapid shifts in depositor sentiment, despite the advances in financial regulation and oversight.

It serves as a modern cautionary tale of the banking sector's vulnerabilities to both economic pressures and the potent force of social media [9].

the Compass View

My two cents (because I know you're desperate to know!)?

The root causes of these events can often be traced back to a combination of regulatory gaps, market overconfidence, and the underestimation of systemic risks. The S&L Crisis, for example, demonstrates the hazards of allowing a financial institution to stray too far from their core competencies into riskier markets without adequate regulatory frameworks or risk management practices in place.

Meanwhile, the recent bank runs illustrate the challenges that digital-era banks face, including the need for robust liquidity management and the importance of maintaining depositor trust in an era where perceptions can shift at the speed of a tweet.

These historical events highlight the critical role of regulatory bodies, like the FDIC, in maintaining the stability of the financial system. They also underscore the importance of continual vigilance, both in terms of regulatory oversight and within banking institutions themselves, to adapt to changing market conditions and emerging risks.

But the vigilance requirement is on you as well. Personally, I deposit my money across different financial institutions diversify my risk profile, much like my investments. This is no different. Everything is in alignment with my personal financial strategy. You may dislike the bigger banks and thing they are greedy (which they are), but they are also least likely to fail because they have friends in high places - this is something to weigh up when considering whether their higher fees are worth it.

V. A Global Perspective: Understanding International Banking Systems

Now, believe it or not, money does exist outside the States, and it behaves differently depending on where you find yourself on the map. When we step outside our local banking comfort zone, the financial landscape can look quite different.

Why should you care, you ask? Because in the ever-shrinking global village, understanding the quirks of international banking isn’t just for the jet-setters, but for anyone who’s ever looked at a currency conversion app or dreamt of owning a little vacation home in Tuscany. The world is becoming more globalised by the minute - staying informed is crucial, even if you don't think it's important now.

Below is a high level teaser on the topic - we will hit Global Financing in more detail in our WIA intermediary modules.

Banking Across Borders

Banking practices and regulations vary as wildly as culinary preferences across the globe. Here's a bite-sized comparison to whet your appetite:

- Regulatory Rigor: In addition to the examples we mentioned in the previous section, places like Germany and Singapore, banks operate under a watchful eye, with regulations tighter than a new pair of shoes. Meanwhile, other locales might take a more laissez-faire approach, letting banks—and your money—breathe a bit easier.

- Account Accessibility: Ever tried opening a bank account in Switzerland? You'll need more than just a smile...unless your name is Jason Bourne. Contrast that with the relative ease in countries like Canada, where banks seem almost as welcoming as a grandmother's house.

- Interest Rates: The land of the rising sun (Japan) has flirted with negative interest rates, essentially charging you to keep your money in the bank. On the other side of the spectrum, countries battling inflation might offer interest rates that look more like phone numbers.

Navigating International Banking

Here are a few pro tips for dealing with the delightful complexities of international banking, because who doesn’t love a challenge?

- Research is Your Best Friend: Before diving into foreign financial waters, do your homework. Understand the banking landscape of your destination country—knowing what you’re walking into can save you a headache (or a heartache) later on.

- Leverage Global Services Wisely: Many banks offer services tailored for international clientele, but tread carefully. Just because it’s labeled ‘global’ doesn’t mean it’s the silver bullet for all your international banking needs.

- The Currency Conundrum: Moving money across borders often involves currency exchange, with rates that can fluctuate as much as your teenager's mood. Keep an eye on trends and consider hedging strategies if you're playing the long game.

- Digital Banking to the Rescue: In a world where borders are increasingly blurred, digital banking platforms offer a lifeline. They can provide real-time insights into your international accounts, but remember, the digital realm knows no borders—so cybersecurity is paramount.

So, with your understanding of the essential functions of banks, on the local and global stages, you might ask what does all this mean for you?

VI. Strategic Banking for Families

If you've made it this far without fantasizing about becoming a hermit to avoid banking regulations altogether, congratulations! You're ready for the next level: finagling family finances without causing a domestic uprising.

Choosing the right banking strategies is akin to selecting the right tools for a crucial home improvement project. The choices you make can either solidify the foundation or leave cracks in your financial structure.

Smart Banking Strategies for Family Financial Wellness

The foundation of family financial wellness lies in how you manage and structure your accounts, and how you instill financial wisdom in the younger generation. The personal strategies provided are examples of how we manage our finances. It's important to evaluate your own financial goals and circumstances when considering these options.

- Joint vs. Individual Accounts:

- Educational Insight: Joint accounts offer couples the ability to pool their resources for common goals, such as saving for a house or family vacations, providing a unified approach to financial planning. Individual accounts, on the other hand, are set up for those that prefer personal expense and investment management, allowing for autonomy and personal financial growth.

- Personal Strategy: My family operates on a "better together" philosophy, channeling our funds into a joint account as a base for our wealth-building strategy. It's not just romantic, it's economically savvy. Merging our funds into a joint account streamlines our financial operations like a well-oiled machine, or at least a moderately maintained family van. Each payday, our funds cascade into this shared reservoir, from which we strategically allocate to various "uses" — refer below for goal specific savings accounts. This approach has not only simplified our financial management but also aligned it closely with our collective goals. But hey, if solo accounts are your jam for a bit of financial independence or secret snack fund, who am I to judge?

- Goal-Specific Savings Accounts:

- Educational Insight: Different savings accounts can be designated for specific purposes, such as education, investments, or emergency funds. This approach ensures funds are allocated and saved accordingly, making it easier to track progress toward each goal. The split to each is tied to your budgeting strategy. Setting up a checking account (a deposit account that is used for everyday spending, pay your bills and transfer money), and a savings account (an account that earns interest and is designed to hold money that you don't plan to spend) as your first bank accounts is a common way to start the journey.

- Personal Strategy: We align our banking with our wealth strategy, segmenting our savings into accounts dedicated to distinct objectives—education savings for the kids, a vacation fund for family adventures, and an emergency stash for unforeseen events, family trust investments and bucket companies (more on this in future advanced modules). And let's not forget the "future tycoons" fund, where we stash away investment capital, teaching the kiddos that money does indeed grow on trees, but only if you plant it in the right soil. This segmentation allows us to visually track our progress toward each goal, reinforcing the tangible benefits of disciplined saving and budgeting. It's a strategy that echoes the broader principles discussed in previous articles on savings and budgeting, applied within the framework of our family's unique aspirations.

- Teaching Financial Responsibility:

- Best Practices: Engaging your spawn in banking from an early age fosters financial literacy and responsibility. Simple lessons in saving, the concept of earning, and the value of money lay the groundwork for savvy financial decisions and less financially induced hair loss in the future.

- Personal Strategy: Our kids might not know how to fold laundry properly, but they're getting a crash course in money management, complete with a high-yield interest rate of chocolate. Because if there's anything that motivates a child, it's sugar. Real cash and education principles might come into play later as they get older, but for now, we're keeping it sweet and simple.

Leveraging Digital Banking Tools

While the digitalization of banking offers unparalleled convenience, it's not without its caveats. It promises to make life easier, and it does—until it doesn't. Here's how to navigate this landscape wisely:

- The Digital Revolution: The advent of online and mobile banking has transformed financial management, offering tools for everything from budget tracking to investment management. Digital wallets and banking apps provide a seamless interface for managing daily transactions and long-term financial planning.

- Risk vs. Reward: While I revel in the convenience of Apple Pay and not having to remember where I buried that emergency $20, I'm not ready to break up with cold, hard cash. Why? Because when the Wi-Fi's down, or some hacker is angry because his grandma kicked him out of the basement, or there's a glitch in the matrix, you can't pay for groceries with digital goodwill. Cash, in its tangible glory, remains king in scenarios where digital falters. We must protect it at all costs.

- Navigating Digital Tools: Utilize digital banking for its strengths—setting custom alerts to monitor spending, using online platforms for budgeting, and exploring digital investment tools for growing your wealth. Yet, always have a contingency plan. And don't just digital tools just because they are there - have a valid reason for using them in terms of supporting your wealth growth, otherwise it just becomes a distraction.

Incorporating these banking strategies into your family's financial plan offers a roadmap to not only safeguarding your finances but also to building a prosperous future. Consider how these insights apply to your household's financial planning.

Are you leveraging joint accounts, goal-specific savings, and digital banking tools to their fullest potential? This might be the perfect moment to have a family finance meeting to discuss and realign your banking strategies with your family's financial goals.

My Closing Thoughts

And there you have it, a whirlwind tour through the enigmatic world of banking, from the comforting confines of local institutions to the daunting depths of international finance.

As we pat ourselves on the back for surviving what might very well be the world’s most thrilling adventure (next to watching paint dry or grass grow), let’s take a moment to reflect on what we’ve learned.

Key Takeaways:

- Interest Rates and Credit Systems: Remember, interest rates are the heartbeats of the banking world, dictating the flow of money with the precision of a Swiss watch (albeit one that occasionally runs backwards). Your credit score, that magical number that determines whether you’re a financial prince or pauper, hinges on your ability to play nice with money.

- Diversity of Banking Types: We’ve discovered that banks come in more flavors than your local ice cream shop, each catering to different tastes and financial appetites. Whether it’s the robust offerings of retail banks, the business savvy of commercial banks, or the digital sleekness of online platforms, there’s a banking sundae with your name on it.

- Banking Regulations and Consumer Safety: Diving into the alphabet soup of regulatory bodies and consumer protection laws, we’ve learned that while the world of banking regulations might not make for blockbuster entertainment, it’s the steel frame that keeps the financial skyscraper from collapsing.

- Strategic Banking for Families: In the digital age, managing family finances is akin to directing traffic in Times Square—requiring nerves of steel and an advanced degree in herding cats. We’ve explored how to leverage joint and individual accounts, the wisdom of goal-specific savings, and the power of digital tools, all while keeping a fond eye on the reassuring solidity of cold, hard cash.

As I keep reminding you loyal readers - you're not navigating this labyrinth alone. Here at the Intelligence Compass, I'm building something more than a collection of financial tips and cautionary tales; I am building a community. A place where questions are encouraged, wisdom is shared, and financial literacy grows stronger with every article.

So, if you do have any questions or thoughts, please reach out and I would be more than happy to support (admin@theintelligencecompass.com).

Looking Ahead: Taxes - The Next Frontier

Ah, taxes, the inevitable sequel in our financial saga. If you thought banking was a rollercoaster, wait until we dive into the thrilling world of taxes in our next instalment of the WIA Basic Module. Brace yourselves for a journey into the heart of financial darkness, where we’ll decode the cryptic messages of tax codes with the enthusiasm of a kid on a treasure hunt (if the treasure were tax deductions and the kid, a very confused adult).

Spoiler alert: it's about as thrilling as a rom-com, but with more paperwork and the ever-looming threat of an audit. Jokes aside, this one is CRUCIAL to understand. All the wealthy people you know and follow, KNOW how to manage taxes to their benefit.

Until then, keep questioning, keep learning!

Please note: The information provided in this article is intended for educational and informational purposes only. It does not constitute professional financial advice. Financial decisions should be made based on your individual circumstances and goals. We recommend consulting with a qualified financial advisor to obtain advice tailored to your specific situation

References

- https://money-gate.com/first-bank-in-world/

- https://www.britannica.com/money/credit-card-companies

- https://robots.net/fintech/how-does-the-banking-system-work/

- https://www.spglobal.com/marketintelligence/en/news-insights/research/the-world-s-100-largest-banks-2023

- https://www.investopedia.com/terms/b/bank.asp

- https://www.federalreserve.gov/supervisionreg/reglisting.htm

- https://www.fdic.gov/regulations/laws/rules/index.html

- https://www.federalreservehistory.org/essays/savings-and-loan-crisis

- https://www.nytimes.com/article/svb-silicon-valley-bank-explainer.html

- https://www.fscs.org.uk/

- https://www.cdic.ca/

- https://www.apra.gov.au/

- https://www.bis.org/bcbs/

- https://www.spglobal.com/marketintelligence/en/news-insights/research/the-world-s-100-largest-banks-2023

- https://corporatefinanceinstitute.com/resources/wealth-management/banking-fundamentals/

Nexus Saga